India Stack – Introduction to Digital Identity and Payments

December 30, 2022

The India Stack is a set of APIs and services that facilitate the delivery of various government and financial services to citizens of India. It consists of several layers, each with its features and functionality. It consists of 4-distinct layers namely presence-less, paperless, cashless, and consent. Here we will focus on the first 3 layers.

Three Layers

Presence-less Layer

The presence-less layer consists of an identity Aadhaar platform, which is a unique identification number issued to all residents of India. Aadhaar enables secure and verifiable online identity authentication, enabling citizens to access various services using their Aadhaar number.

Paperless Layer

The electronic Kow Your Customer (e-KYC) allows for the electronic verification of an individual’s identity using their Aadhaar number. This process is used to verify the identity of customers when opening new bank accounts, applying for loans, and other financial transactions. eSign (electronic signature) enables citizens to digitally sign documents and contracts using their Aadhaar number. This allows for the secure and convenient completion of various transactions and agreements online. DigiLocker is a digital repository for storing and sharing documents securely. Citizens can use their Digital Locker to store and share important documents, with government agencies and other organizations. It includes a driver’s license, passport, birth certificate, etc.

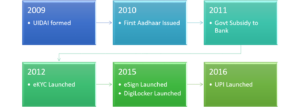

Timeline of Introduction

With the rollout of Aadhaar in 2010, NPCI launches Aadhaar enabled payment system to channel government subsidies directly into Aadhaar-linked bank accounts in 2011. UIDAI introduced electronic Know Your Customer (eKYC) that brought down the cost for banks by over 150x. The Controller of Certifying Authorities (CCA) launches eSign as an open API allowing Aadhar holders to digitally sign any document. Ministry of Electronics and Information Technology (MeitY) launches the Digilocker platform for the issuance and verification of documents & certificates digitally, thus eliminating the use of physical documents.

Cashless Layer

This layer refers to the various technologies and systems that enable individuals and businesses to make and receive payments digitally. The cashless layer consists of several products, including the Unified Payments Interface and the Aadhaar Enabled Payment System. To learn more on the examples of implementations refer to The India Stack Reference – 2022 and Beyond – (grepdigital.com).

Unified Payment Interface (UPI)

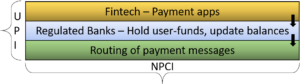

UPI is a real-time payment system that allows individuals and businesses to make and receive payments using their mobile phones. UPI allows for the seamless transfer of funds between bank accounts without needing additional authentication or payment gateways. Various banks and financial institutions support UPI in India. Google Pay, PhonePe, and Paytm provide an interface to UPI. It enables interoperability between money custodians, payment rails, and front-end payment applications. UPI operates on a shared infrastructure model, where multiple banks can participate and offer UPI services to their customers. This allows users to make payments to any bank account in the country, regardless of which bank they are a customer of.

UPI is a payment markup language that runs on a central switch operated by NPCI. It is a bank-owned non-profit organization. In simple terms, all the licensed banks connect to the NCPI server. This server sends messages to and fro between all the banks, with NPCI as the middleman.

Benefits of UPI

- The superiority of the end user experience when compared with digital wallets, card networks, or traditional bank transfers.

- UPI obviates the need to fund any kind of intermediary wallet and provides interoperable payment rail. Users can make real-time payments directly in and out of their bank accounts, at essentially no cost.

- UPI also makes use of a separate UPI PIN as a means of second-factor authentication. It supports a Virtual Payment Address (VPA) in addition to typical identifiers like bank account numbers or debit card CVV. It provides a more flexible and secure payment experience when compared with alternatives.

- UPI apps allow consumers to make payments via QR codes as well. This allows any UPI-enabled application to account for all the online and offline payment requirements of an Indian user.

- Beginning of 2020, UPI extended support for auto-payments that provide its users with the ability to ascribe standing instructions (time, day, regularity, etc) for their recurring payments.

UPI empowers every Indian with a smartphone to participate and transact in the digital economy. It has also laid the foundation for several innovations in India’s payments artillery.

Aadhar Enabled Payment System (AEPS)

AEPS is a payment system that allows citizens to make and receive payments using their Aadhaar number and biometric authentication. AEPS enables secure and convenient financial transactions for individuals who do not have access to credit or debit cards. Banks and financial institutions in India support AEPS. Users can access it through AEPS-enabled point-of-sale (POS) terminals and micro ATMs.

Features of AEPS

- Aadhaar-based authentication: AEPS uses the unique Aadhaar number and biometric authentication of an individual to verify their identity and enable financial transactions. This provides a secure and convenient way to identify and authenticate users, without the need for additional documents.

- Multiple transaction types: AEPS enables a range of financial transactions, including cash withdrawal, balance inquiry, and cash deposit. This allows individuals to access a variety of financial services using AEPS.

- Inclusive access: AEPS is designed to be accessible to individuals who may not have access to other forms of payment, such as credit or debit cards. It enables financial transactions for individuals who cannot use traditional payment methods due to illiteracy or lacking access to technology.

- Convenience: AEPS allows individuals to make and receive payments using their Aadhaar number and biometric authentication, which is convenient and easy to use. AEPS-enabled POS terminals and micro ATMs are available in various locations. This includes banks, post offices, and retail outlets, making it easy for individuals to access AEPS services.

Benefits of AEPS

- Increased financial inclusion: AEPS enables individuals who may not have access to other forms of payment to participate in the formal financial system. This can help to increase financial inclusion and reduce the use of cash, which can have a range of benefits, such as reducing the risk of fraud and improving financial transparency.

- Convenience: AEPS is convenient and easy to use, making it accessible to many individuals. It allows individuals to make and receive payments using their Aadhaar number and biometric authentication, which is simple and easy to use.

- Security: AEPS uses Aadhaar-based authentication, which is secure and reliable. This helps to protect against fraud and unauthorized access, providing a secure way for individuals to make and receive payments.

- Efficiency: AEPS can help to streamline financial transactions and reduce the time and effort required to complete them. This can help to increase efficiency and reduce the cost of financial transactions, benefiting both individuals and businesses.

Types of Payment Apps

In the payments layer, several technologies have been introduced over the years to facilitate digital payments in India. Some of the notable ones are:

- BharatQR: This is a common QR code standard that enables merchants to accept digital payments from various payment instruments, such as debit and credit cards, UPI, and mobile wallets. It simplifies the payment process by eliminating the need to manually enter payment details.

- India Post Payments Bank (IPPB): This is a bank that provides a range of financial services, including accepting deposits, issuing debit cards, and facilitating digital payments, through a network of post office branches across the country.

- National Electronic Toll Collection (NETC): This is a system that enables electronic toll payment at national highways using RFID (Radio Frequency Identification) technology. It eliminates the need for toll booths and reduces the time and hassle of toll payment.

- e-NAM (National Agricultural Market): This is an online platform that connects agricultural produce mandis (wholesale markets) across the country and enables farmers to sell their produce directly to buyers without intermediaries. It also facilitates digital payments through UPI and other instruments.

- Bharat Interface for Money (BHIM): BHIM is a digital payment app that allows users to make and receive payments using UPI. National Payments Corporation of India (NPCI) drives the development and support and is available on both Android and iOS platforms.

Many private players leveraged the UPI system to provide payment services. They include Paytm, Google Pay, and PhonePe apps which offer a digital wallet and online payment system that allows users to make and receive payments, as well as shop online. It is available on both Android and iOS platforms.

Summary

The presence-less, paperless, and payment layers of India Stack play a crucial role in enabling the digital transformation of government and financial services in India.

- Enables the creation of a digital identity for every resident of India

- Reduces the reliance on physical documents and enabled the efficient exchange of information between individuals and organizations

- Improves the speed of the delivery of various financial services in India, including the ability to send and receive payments digitally.

Overall, the India Stack contributes significantly to the growth of digital payments and the reduction of reliance on physical documents in the country. It opens up opportunities for different players to participate in the growing economy offering customized solutions at more affordable rates.

Grep Digital has used the India Stack extensively to build identity, and payments solutions. Connect with us to partner in your adoption of the India Stack and build seamless solutions.

Credits: https://indiastack.org

Insights

Tag Cloud

- API & Automation

- Artificial Intelligence

- Business Process

- Cloud

- Cognitive

- Contact Center

- Cybersecurity

- Data Engineering

- DevOps

- Digital Transformation

- Dynamic Teams

- E-Governance

- Enterprise Apps

- Fractal Teams

- GenAI

- Green Engineering

- IIoT

- Interaction Design

- Low Code

- Microsoft Apps

- Mobile Apps

- SaaS

- SDLC Practices

- Sustainability

- UI/UX

- Web3

- Workflows